The Week That Had Everything — Your Full Breakdown Inside

UpsideTrader Weekend Market Report — Week of April 28 – May 2, 2026

What a week. By Friday’s close, you’d be forgiven for forgetting how ugly things looked in the middle of it. The S&P 500 finished at 7,230, the Nasdaq hit 25,114 — a brand new all-time high — and both indexes posted their best monthly returns since 2020 in April, gaining roughly 10%. But to understand where we are heading into next week, you have to understand the full story of how we got here, because this week had everything: a Fed meeting, four Magnificent Seven earnings in a single night, an Iran peace signal, and Apple closing out the week with a bang.

Monday/Tuesday — The OpenAI Scare

The week opened on shaky ground. A Wall Street Journal report dropped suggesting OpenAI had missed its own internal revenue and user growth targets, with CFO Sarah Friar reportedly warning leadership that the company might struggle to pay its computing contracts if the top line didn’t accelerate. That was enough to send chips and AI-adjacent names into a tailspin. Nvidia, AMD, Broadcom, and CoreWeave all took hits. Oracle dropped more than 5%. The Nasdaq shed nearly 1% on Tuesday, and the mood turned cautious just as earnings season was about to peak.

Adding fuel to the fire, the UAE announced it was leaving OPEC effective May 1, a seismic development in the oil markets that nobody saw coming. Oil had already been running hot on the Iran conflict and the Strait of Hormuz situation — WTI briefly crossed $100 a barrel during the week, while Brent touched $112. Gas at the pump hit its highest level since August 2022.

Wednesday — The Fed and the Big Tech Earnings Tsunami

Wednesday was one of those days you don’t see often. The Fed held rates steady at its meeting, as expected, but the 8-4 vote showed real internal division — Powell is navigating sticky inflation (core PCE at 4.3%) against an economy that actually grew at 2% in Q1, a solid rebound from the 0.5% print in Q4. AI investment was cited as a meaningful contributor to that GDP number, which tells you something about where we are in this cycle.

Then, within roughly 80 seconds of the closing bell, Microsoft, Alphabet, Amazon, and Meta all reported earnings simultaneously. Here’s how it shook out:

Microsoft beat on EPS, coming in at $4.27 against estimates of $4.06. Azure held its growth trajectory and the stock responded well. Alphabet was the standout of the night — their AI monetization story is working, cloud revenue impressed, and the market rewarded them for it. Amazon delivered on AWS growth, which came in strong, and retail margins continued to improve. Meta was the odd one out. Revenue came in at $56.3 billion, up 33% year over year, and net income surged 61% to $26.8 billion — so the headline numbers were actually excellent. But investors zeroed in on capex, which continues to balloon, and on Meta’s AI ROI story, which isn’t as clean as Alphabet’s. The stock got a more muted reception as a result. The theme is clear going into next quarter: the street is demanding better AI return-on-investment disclosure, and the companies that can provide it will be rewarded while those that can’t will be punished regardless of the top-line numbers.

Thursday/Friday — The Recovery and Apple’s Moment

Thursday saw a powerful reversal, with the Dow surging more than 790 points as communication services and industrials led the charge. Easing oil prices helped — there were reports filtering through Pakistani mediators that Iran had sent a new peace proposal. Nothing confirmed, nothing signed, but enough to take the geopolitical premium off crude and lift sentiment across the board.

Then Friday was Apple’s moment. The company posted a strong fiscal Q2 earnings and revenue beat, with forward guidance that quieted the iPhone demand bears. Apple climbed more than 3% and pulled the Nasdaq to 25,000 for the first time ever. It was the perfect capstone to a chaotic week.

What to Watch Next Week

Nonfarm payrolls hit on Friday and will be the main macro event. The labor market has been sending mixed signals, and with inflation still sticky and the Fed divided, a strong number could reignite rate-hike fears, while a weak one could raise recession concerns. Neither is a clean outcome.

On the earnings front, PLTR, AMD, and ARMH all report — three names that sit right at the intersection of the AI trade. After the OpenAI scare early in the week and the mixed signals from Meta, these reports will matter. Berkshire Hathaway reports this weekend as well, and Buffett’s commentary on the macro environment will be worth reading closely.

One more thing worth flagging: Powell’s term as Fed chair ends May 15, and Kevin Warsh’s nomination advanced through the Senate Banking Committee along party lines this week. The transition at the Fed, happening right in the middle of an active geopolitical conflict and sticky inflation, is a wildcard that the market hasn’t fully priced in yet. Keep that in the back of your mind.

Here are some thoughts. I don’t think anyone knows where crypto is going; that’s why I watch charts, because it squeezes out the white noise and opinions. And pattern recognition on charts is usually very helpful.

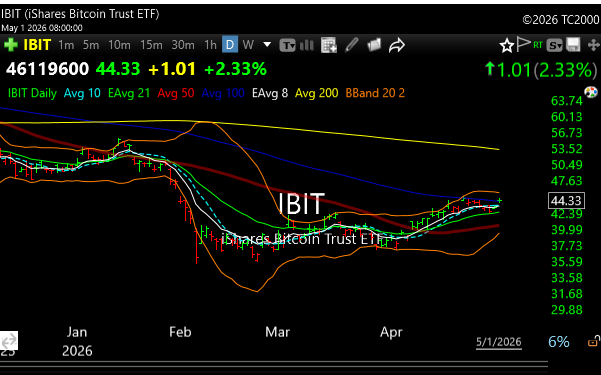

Bitcoin..IBIT is now above some very key moving averages. The 200 DMA above is the only one left, and it comes in at around $53.31. The chart seems to be setting up. BITX is 2X IBIT.

MSTR broke out of a tight bull flag on Friday. The chart is very constructive. MSTU (2X MSTR) has a viciously bullish tight bull flag on the weekly chart that is also broke out on Friday.

Most of the setups I love are reporting earnings next week, so I will avoid. That’s a 50/50 prop, so I’m off the trades for now.

LAES– A quantum name that we more than doubled on a year ago. It has pulled way back, but is setting up again. I didn’t sell from 3 to 8, dumb in hindsight, but added some more around these prices last week. Not a fast trade. Quantum stocks are starting to look ready again, so this one is only as good as the market and a “risk on” tape.

ARKK– Kathy Wooed is flagging hard. TARK is the 2X long ETF, also flagging hard.

The question now is whether May can build on this action or whether the wall of worry starts to win. See you in the morning.

Breaking news: Trump evidently opened the Strait for most, with the exception of Iran. Its been confirmed but details are evolving.