Dow -279.13 at 44371.51, Nasdaq -45.14 at 20585.53, S&P -20.71 at 6259.75

The announcement of a 35% tariff on Canadian imports, the indication that the EU will be getting a tariff letter, and the president’s assertion that most trading partners will face a 15% to 20% tariff rate triggered the market’s worst open this week. The initial selling, however, did not persist. The mega-cap stocks led a rebound from the opening lows and helped the indices settle into a sideways drift below their unchanged lines for the majority of the session. The market has been generally unfazed by tariff headlines over the past week; sure, there were days with some early session profit taking, but these were often on the heels of strong closings.

Big Bank and Tech Earnings Set the Tone for the Week

The second-quarter earnings season kicks off with major banks and tech giants reporting. Investors are watching closely to see if companies can navigate the shifting trade landscape and maintain profit growth.

Fed Policy in Focus Amid Inflation and Tariff Concerns

The Federal Reserve remains on hold, with officials citing tariff-driven inflation risks as a reason for caution. Markets are pricing in a possible rate cut in September, but policy direction is still uncertain.

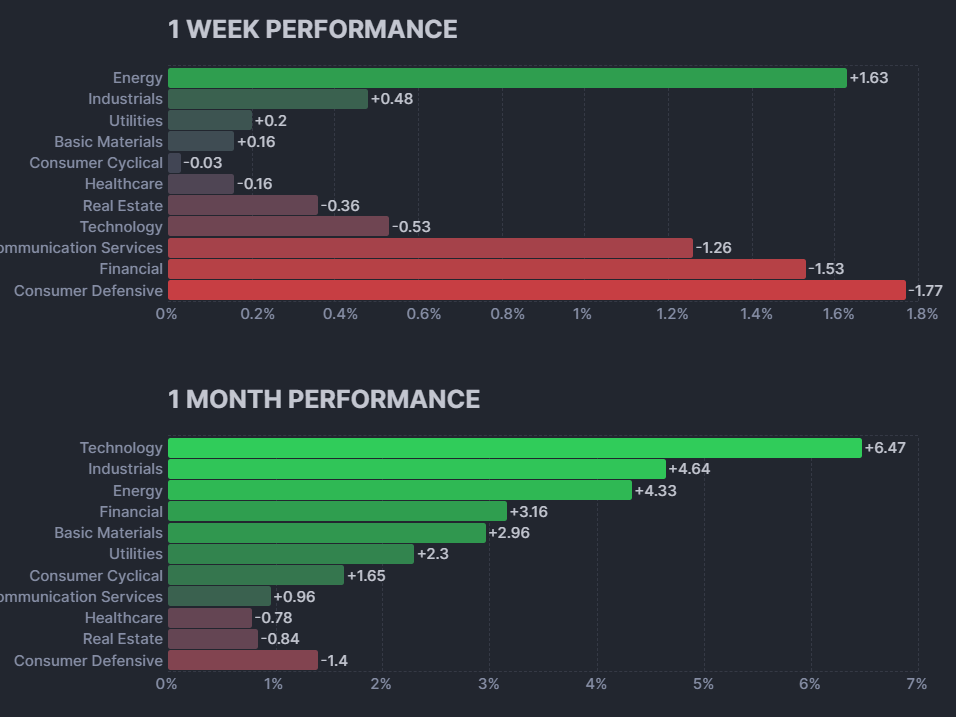

AI and Tech Stocks Remain a Bright Spot

Despite broader market caution, leading technology names like Nvidia and Micron continue to outperform, driven by robust demand for AI and semiconductor products. Their growth is helping to underpin the resilience of the Nasdaq and tech sector overall.

Here’s how things are going in Bitcoin land for the shorts……….

Earnings are starting again. Next week, we also have VIX expiry and July Opex, so we could see some volatility. Some setups are coming..